Pulse24 Original

Gold's 30% Correction: A Story About Inflation, Oil, The Dollar and Changing Expectations

Gold has fallen sharply from its highs.

After trading near $5,580 earlier this year, it now hovers around $4,000, a correction of roughly 30%.

Gold didn't fall because the long-term case for gold disappeared.

It fell because the market changed the story it was pricing.

At the start of 2026, investors believed the macro environment was finally turning in gold's favour.

The expectation was straightforward: the Federal Reserve would begin cutting rates, the U.S. dollar would weaken, liquidity would improve, and non-yielding assets would outperform.

In that environment, gold wasn't simply an inflation hedge. It became a bet on easier money.

That belief drove one of the strongest rallies in recent years. Gold climbed from roughly $2,700 in late 2025 to nearly $5,580 in early 2026.

But that rally depended on one assumption. Inflation had to continue falling.

Instead of cooling, inflation remained stubborn. Oil became the catalyst. Crude climbed toward $100 per barrel, feeding into transportation costs, manufacturing input prices and broader inflation expectations.

The market that had been positioned for multiple rate cuts suddenly had to price a different reality. What if the Federal Reserve couldn't cut rates as quickly as expected?

That question marked the beginning of gold's correction.

The Biggest Misunderstanding About Gold

Many investors believe gold automatically rises whenever inflation rises. That isn't entirely true.

Gold performs best when inflation is high but real yields are falling, or when investors believe central banks are losing control of inflation.

However, if inflation remains elevated and the Federal Reserve keeps interest rates high, the picture changes completely. Real yields remain positive. And positive real yields become one of gold's biggest headwinds.

Gold pays no coupon, no dividend, no yield. When investors can earn attractive real returns by holding Treasury securities or cash, the opportunity cost of holding gold increases. That is why higher-for-longer monetary policy often weighs on gold, even during periods of elevated inflation.

The mechanism was surprisingly simple: sticky inflation delays Federal Reserve rate cuts, which keeps Treasury yields elevated, which keeps real yields positive, which strengthens the U.S. dollar, which causes gold to lose momentum.

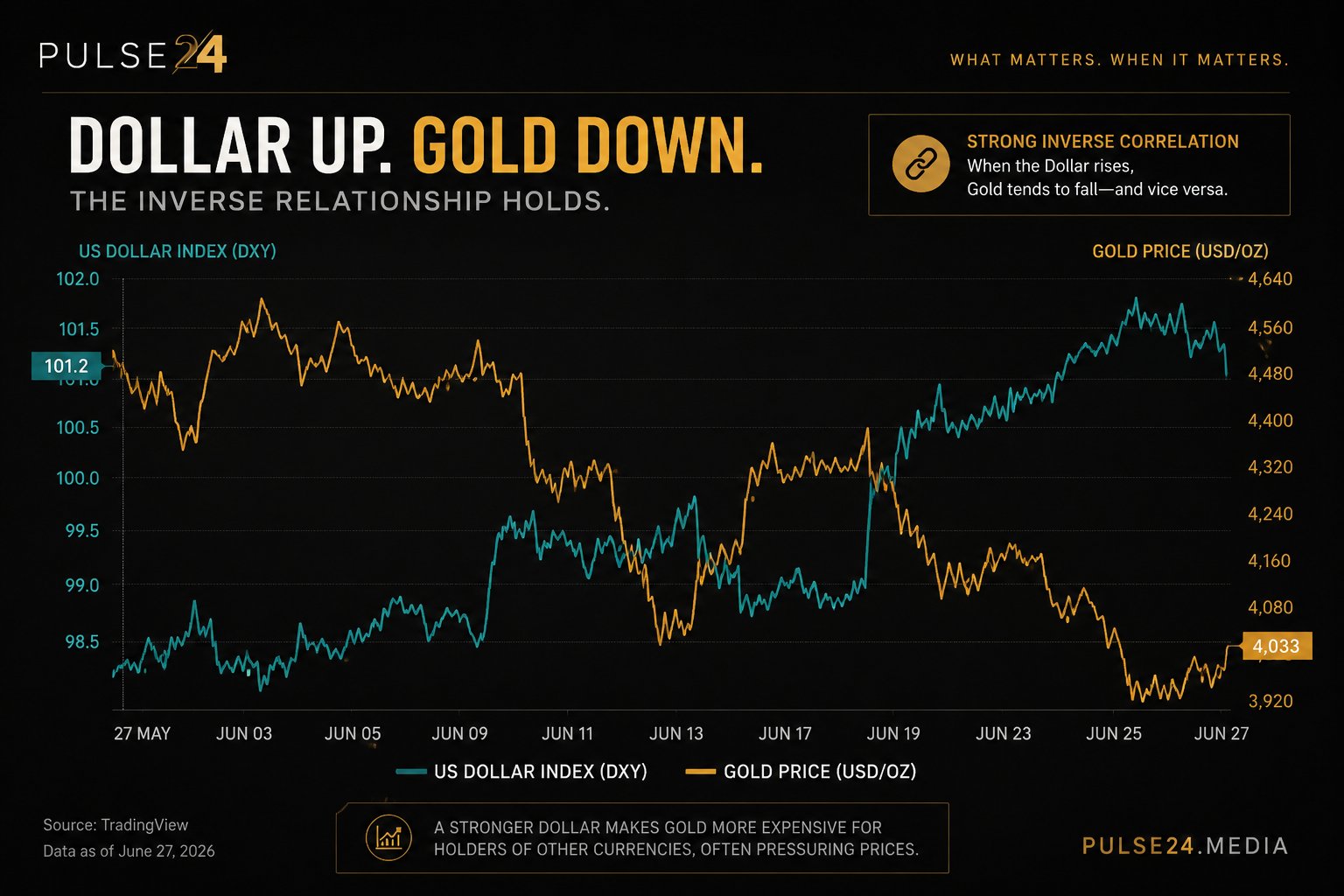

Gold's correction wasn't random. It was the market repricing an entirely different macro regime. As expectations for Federal Reserve easing faded, the U.S. dollar strengthened, and that matters for two reasons.

First, gold is priced in dollars. A stronger dollar makes gold more expensive for international buyers, reducing demand outside the United States.

Second, dollar strength usually reflects tighter financial conditions, and tighter financial conditions rarely provide a supportive backdrop for gold.

Positioning Made The Correction Worse

Gold entered 2026 with nearly every bullish factor aligned: central bank buying, ETF inflows, safe-haven demand, inflation concerns, and expectations for lower interest rates.

When one of those pillars collapsed, the expectation of imminent rate cuts, the positioning that had fuelled the rally also accelerated the decline. Markets don't simply move because fundamentals change. They move because expectations change.

Many investors pointed to continued central bank purchases as a reason gold couldn't fall significantly. The long-term thesis remains valid. Emerging-market central banks continue diversifying reserves and reducing dependence on the U.S. dollar.

But central bank buying operates over months and years. Financial markets move in hours. ETF outflows, futures positioning and institutional portfolio adjustments overwhelmed the slower pace of official-sector demand. That doesn't invalidate the structural case for gold. It simply explains why structural buyers couldn't prevent a cyclical correction.

Ironically, the same commodity that helped trigger gold's correction may eventually support its recovery. Oil has already declined from roughly $97 to around $72 per barrel in less than a month.

Lower energy prices reduce inflationary pressure throughout the economy. If inflation continues easing over the coming months, markets may once again begin pricing Federal Reserve rate cuts. That would reduce upward pressure on real yields, and it could also weaken the U.S. dollar. Both developments would improve the macro backdrop for gold.

There isn't one path forward. There are three.

Scenario One, bullish for gold: inflation continues falling, rate-cut expectations return, real yields decline, the dollar weakens, and gold benefits.

Scenario Two, neutral: inflation remains sticky, the Federal Reserve maintains higher rates, real yields stay positive, dollar strength persists, and gold struggles to rebuild momentum.

Scenario Three, risk-off rally: economic growth deteriorates while inflation remains elevated, markets begin searching for safety, and gold could recover through safe-haven demand, although the path would likely be far more volatile.

Gold's correction isn't simply a commodity story. It is a story about changing macro expectations: oil feeding inflation, inflation delaying Federal Reserve easing, higher real yields supporting the dollar, and investors unwinding positions built for a completely different environment.

Gold hasn't lost its long-term relevance. The market simply stopped pricing the world that had carried gold to its highs.

And until that macro regime changes again, gold will continue responding less to headlines and more to the direction of inflation, real yields and the U.S. dollar.

How we read the data

Curious how we get from raw data to a take like this? Our Trader's Toolkit walks through the tools we lean on.

Explore the Toolkit