Pulse24 Original

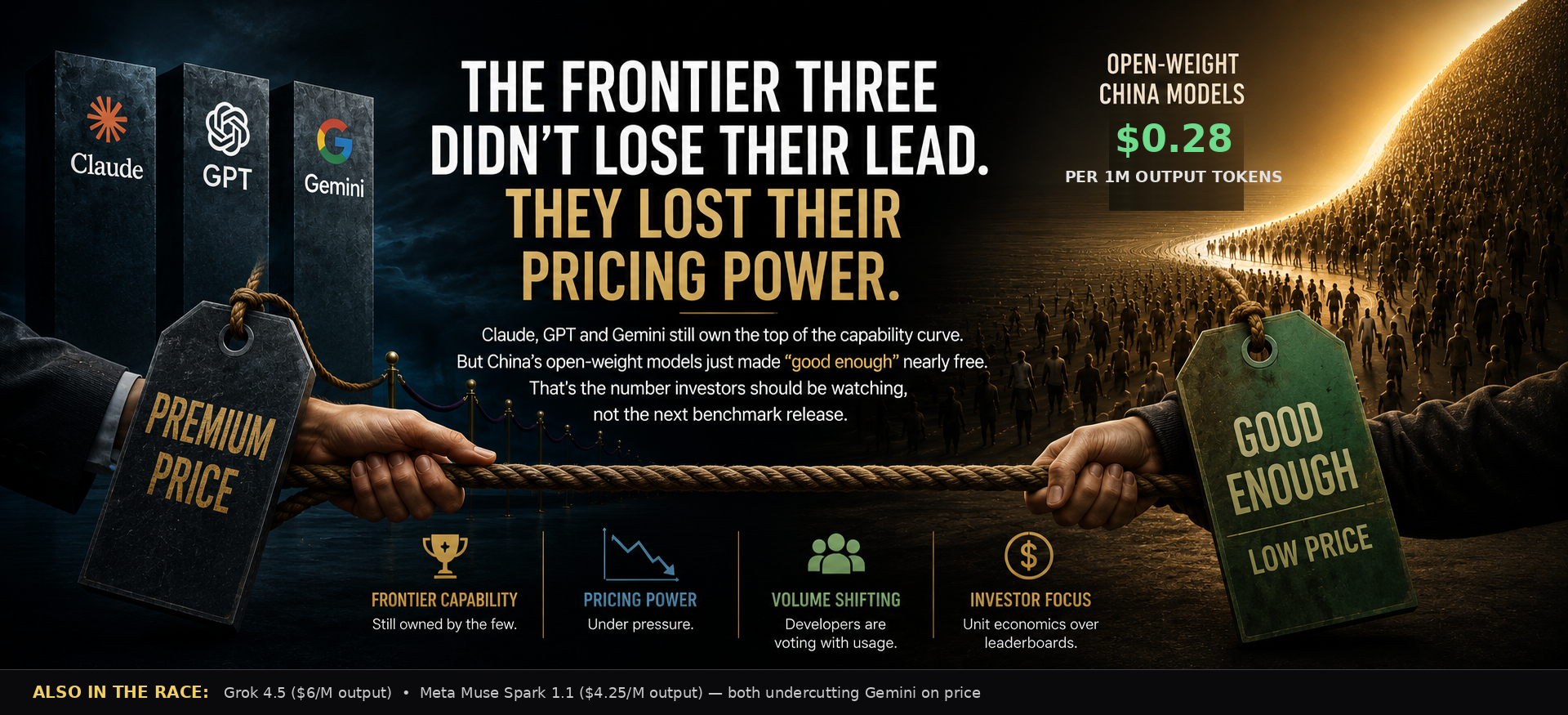

The Frontier Three Didn't Lose Their Lead. They Lost Their Pricing Power.

Claude, GPT and Gemini still own the top of the capability curve. China's open-weight labs, and a widening field of cheaper US challengers, just made "good enough" nearly free. That's the number investors should be watching, not the next benchmark release.

July 17, 2026

The market is asking the wrong question. Everyone wants to know who has the smartest AI. Investors should be asking who still has the power to charge a premium for it, and those two questions are quietly coming apart. The market is still rewarding intelligence leadership as though pricing power automatically follows. History says those two things tend to separate long before anyone's ready for it.

Claude, GPT and Gemini still sit at the top of the capability curve, and nothing here argues otherwise. What's changed is how many directions the pressure on their pricing is now coming from.

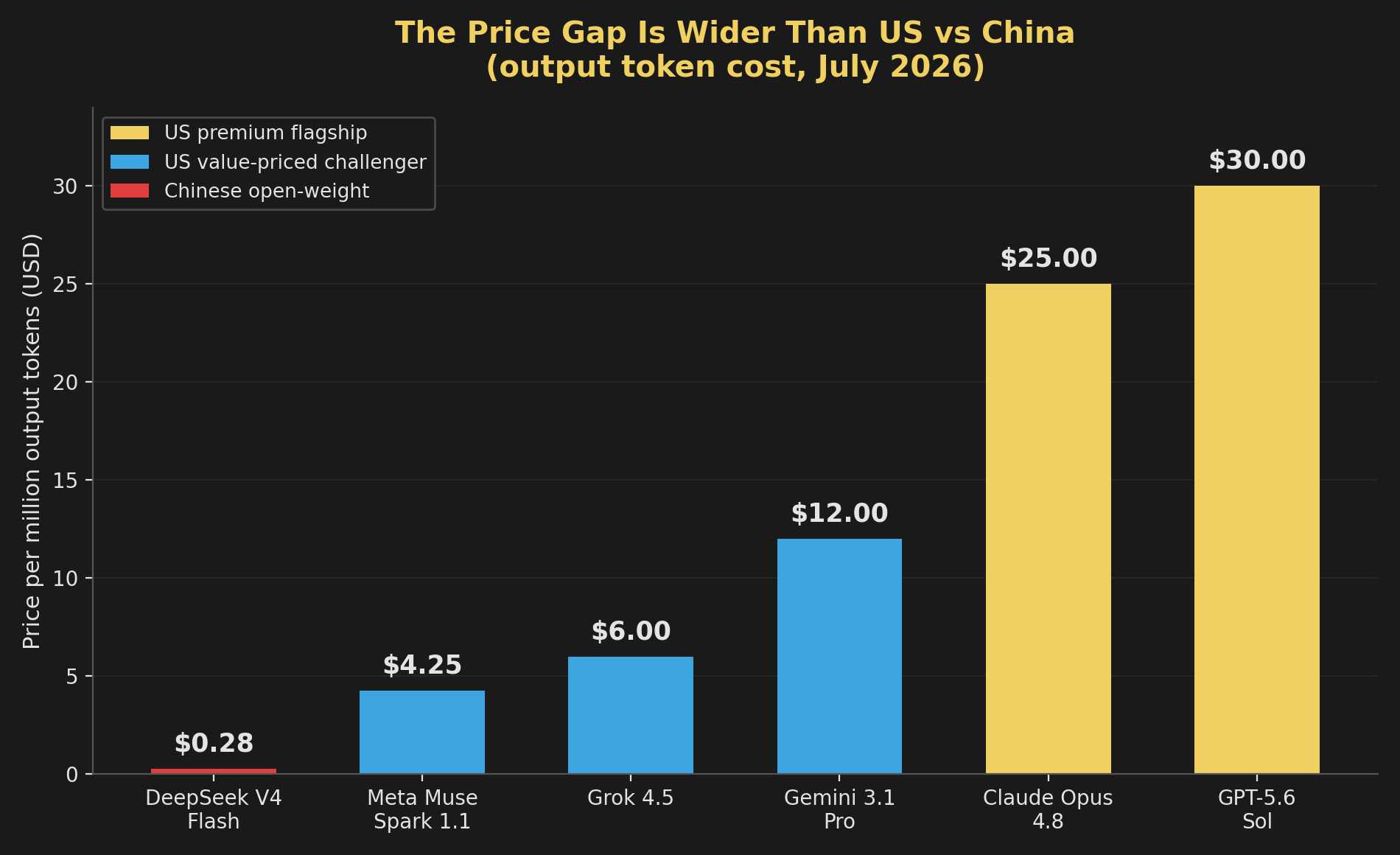

Claude still owns coding, and that's probably the hardest lead to attack, because software engineering rewards reliability more than almost anything else. On SWE-bench Verified, the test of whether a model can fix a real bug end to end, Anthropic's models take the top three spots industry-wide. Gemini isn't trying to win that fight. It's quietly becoming the default choice for anyone running reasoning at volume. Part of that is cost. It runs around $12 per million output tokens against $25 to $30 for its two closest rivals, and it doesn't give up much on Google's own science benchmarks to get there. GPT is chasing a third thing entirely, the hardest math and science problems that exist, where it leads by roughly double the next-best score on FrontierMath Tier 4.

None of the three bets are free. Claude costs the most to run at scale, which is fine if reliability is what you're paying for and expensive if it isn't. Gemini still trails on the hardest structured reasoning chains despite its broader science lead. GPT's newest tier launched behind a gated preview tied to a government safety review and now carries the highest price of the three, a gap that's really about access more than ability.

Then two more labs showed up in the same week, and that part is easy to miss if you're only tracking three names. xAI's Grok 4.5 landed July 8 at $2 input and $6 output per million tokens, about a quarter of Opus 4.8's price, scoring 64.7% on SWE-bench Pro against Opus's 69.2% and actually beating it on Terminal-Bench, a test of multi-step command-line execution. Musk called it "roughly comparable to Opus 4.7, but much faster," a more careful claim than the usual launch-day framing, though most of Grok 4.5's numbers are still self-reported this early and worth treating that way. Meta's Muse Spark 1.1 followed a day later out of the Superintelligence Labs group Alexandr Wang built after the Scale AI deal, priced at $1.25 and $4.25, closed-weight for the first time in Meta's history despite Llama's open-source legacy. It trails badly on coding but is actually ahead of Opus on agentic tool use and document reasoning.

Neither model threatens the top of the capability curve, not yet anyway. Both make it a lot harder to justify what sits at the top of the price list, which is really the point. Nobody needs to dethrone Claude, GPT or Gemini on raw intelligence to change how this market gets priced. They just need to be good enough at a quarter of the cost, and now there are two more doing exactly that.

We've seen this movie before

Nvidia still builds the fastest AI chips, and most inference workloads don't need them. Google, Amazon and a handful of others already run meaningful production volume on custom silicon at a fraction of the cost, because most of what's running doesn't need the ceiling, just enough of it.

Every technology matures the same way eventually. One business owns performance. Another owns volume, and volume is where the money ends up sitting once the novelty wears off. AI is getting there faster than most people modeling these valuations expected, and this time the pressure is coming from two directions at once instead of one.

The number that actually moves valuations

Chinese-origin models have held more than 30% of weekly token volume on OpenRouter, the largest AI model routing platform, every single week since February. By early July that share hit 46%. A year earlier it was under 5%. That's not sentiment. That's production traffic, and production traffic doesn't lie the way a survey or a sentiment index can.

It isn't loyalty, it's arithmetic. DeepSeek's V4 Flash runs $0.28 per million output tokens, cheaper than Muse Spark's $4.25 and Grok's $6, both of which are themselves a fraction of Claude Opus 4.8's $25 and GPT-5.6 Sol's $30. One automation startup told CNBC it moved its entire traffic load from Claude to DeepSeek and expects to save millions a year. Another saw usage of a Chinese model jump 27-fold in a single week after switching. When a task doesn't need the best model, and increasingly it doesn't, it goes to whichever one clears the bar for the least money. That calculus doesn't care which flag is on the model card.

Timing didn't help. When Anthropic's most capable models went dark in June under a US export control order, some enterprises had no transition plan and no fallback ready. A few moved to Chinese alternatives out of necessity and simply stayed once they saw what it cost to run production traffic that way. The regulation didn't start the shift toward cheaper models. It forced a decision a lot of companies were already circling into a single afternoon for a handful of large users.

Why the gap closed faster than anyone priced in

Claude's top model still scores 95% on SWE-bench Verified against the high 70s and low 80s for the best Chinese open-weight models. That's a real gap, but it's nothing like where things stood eighteen months ago, back when DeepSeek's R1 first proved a Chinese lab could match Western reasoning quality at all. Alibaba's Qwen family is now the single most-downloaded open-weight model line on Hugging Face on the planet, built on distribution more than any headline benchmark score, and four of the five most-used open-weight models globally are Chinese today. That lineup simply didn't exist two years ago, and the pace of it catching up is arguably the more important number than where it currently sits.

Money doesn't disappear. It moves.

Hyperscalers keep their cut regardless of who wins, since AWS, Azure and Google Cloud get paid for the compute whether it's running Claude, GPT, Gemini, Grok, Muse or DeepSeek underneath. Software companies that wrap AI into a finished product can price on the outcome the product delivers instead of the tokens it burns getting there, which insulates them from whatever's happening one layer down. Routing platforms like OpenRouter take a toll on volume no matter whose model happens to be fashionable that quarter, and volume is the one thing all of this is increasing for everyone involved.

The application layer might end up the real winner here, and it's worth spelling out why. Cheaper intelligence is just an input cost to a business actually solving someone's problem with it, and falling input costs tend to grow that business rather than shrink it. A customer support tool that used to eat its margin on Opus-tier API calls suddenly has room to expand into a market it couldn't have served profitably a year ago. That's not a hypothetical, it's the same mechanism that made cheap cloud compute turn into a thousand internet businesses that couldn't have existed at 1990s server prices.

Why this matters for investors

If pricing compresses across the middle of the market, revenue can keep growing and usage can keep climbing while margins quietly decline underneath both numbers. Investors often mistake revenue acceleration for durable pricing power. They are not the same thing, and conflating them is exactly how a market gets a valuation wrong for a year or two before the correction shows up all at once.

The next two quarters will tell us more than the next benchmark release. Watch what happens to API pricing on the frontier three's mid-tier models specifically, not their flagships, since that's where the real volume actually sits and where a quiet cut would show up first. Watch whether Grok and Muse convert this month's benchmark claims into real enterprise contracts once someone outside xAI and Meta has independently verified the numbers, because self-reported scores in launch week and sustained enterprise adoption six months later are two very different tests. None of this means the frontier labs are losing the AI race. It means staying ahead on intelligence and staying ahead on margin have quietly become two separate jobs, and only one of them shows up in a benchmark leaderboard.

Technology leadership creates headlines. Pricing power creates shareholder returns. The next phase of AI may be decided by the second, not the first.

How we read the data

Curious how we get from raw data to a take like this? Our Trader's Toolkit walks through the tools we lean on.

Explore the Toolkit