Pulse24 Original

AI Infrastructure Won the First Trade. Distribution Could Win the Second.

AI investing has mostly been a bet on who builds the infrastructure and who wins the model race. There's a quieter third layer, the companies that already own the audience, and the economics there work completely differently.

July 14, 2026

For two years, AI investing has revolved around one question: who builds the future. It's a fair question. Who builds the chips, who trains the biggest models, who owns the compute, who can afford another $100 billion data center. That's where almost all of the capital has gone, and for good reason. Without Nvidia's GPUs, TSMC's fabs, Broadcom's networking, or the frontier labs pushing model capabilities every few weeks, none of what we're seeing today would exist.

But lately I've found myself wondering whether we're all looking at only two-thirds of the story. Building AI and owning the customer aren't the same business, and markets have a habit of eventually rewarding both.

AI Isn't One Trade. It's Three.

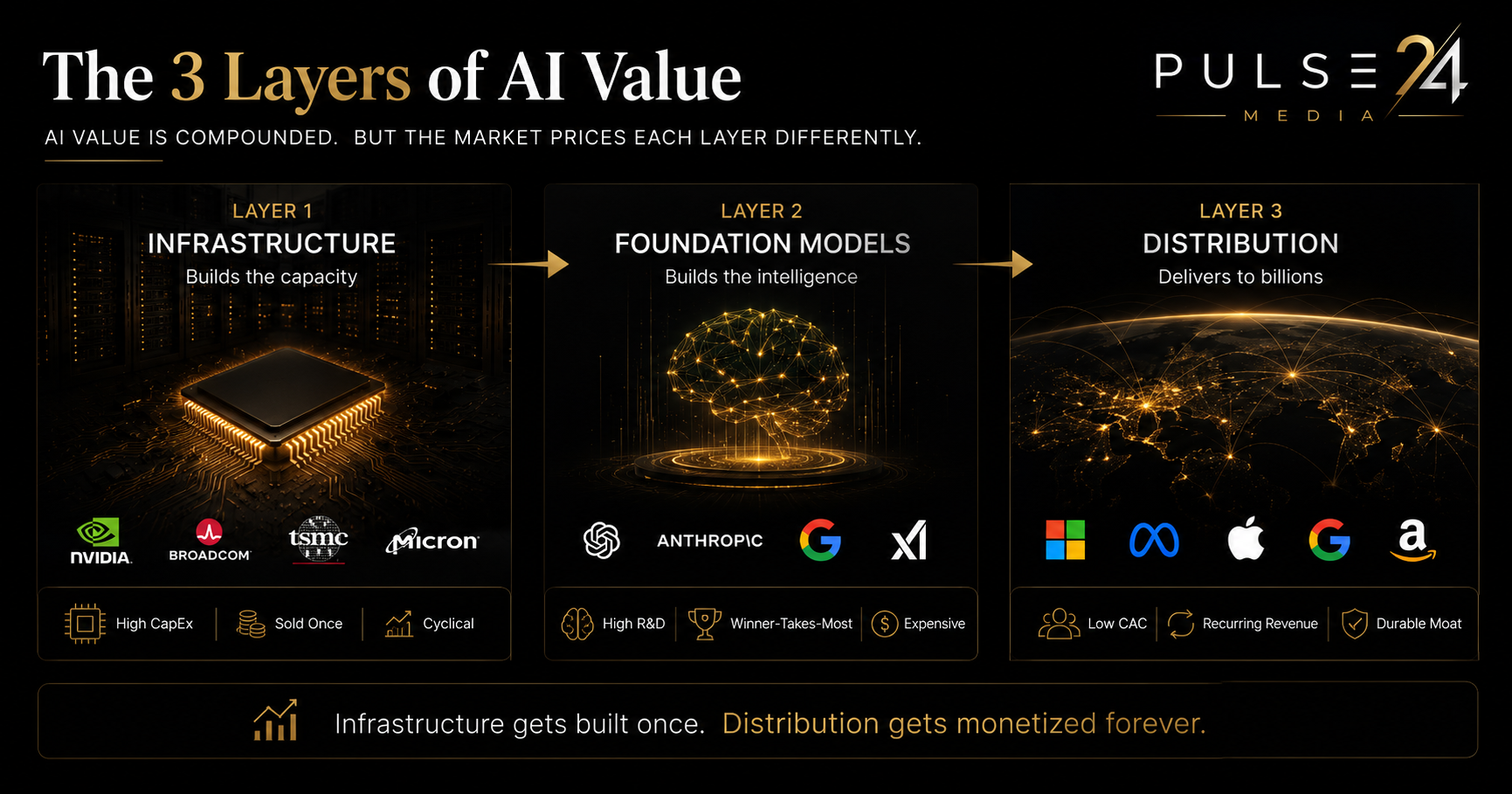

One mistake I think investors make is putting every "AI stock" into the same bucket. They're not. There are really three different businesses hiding inside what we casually call the AI trade.

Layer one is infrastructure, the companies selling the picks and shovels. Nvidia, Broadcom, TSMC, Micron, the power suppliers and networking companies. Everything the AI economy physically runs on.

Layer two is intelligence, the companies competing to build the smartest models. OpenAI, Anthropic, Google DeepMind, xAI. This is the layer everyone watches. Every few weeks another benchmark falls, another model takes the lead, another launch reshuffles expectations. Leadership here can change remarkably fast.

Layer three is distribution, and this is the quiet one. Microsoft, Meta, Apple, Google, Amazon. These companies already sit inside billions of people's daily routines. Whether the best model this month comes from OpenAI, Anthropic or xAI almost becomes secondary if your product is already where people spend their time. That's a very different competitive advantage.

The Market Has Been Pricing The Buildout

Infrastructure deserved the attention, and it still probably does. Demand continues to surprise, capex keeps moving higher, and every major cloud provider is still racing to add compute faster than customers seem willing to consume it. The investment case has been obvious. If AI demand explodes, someone has to sell the hardware, and markets rewarded that, understandably.

But here's the question I don't think gets asked often enough. What happens after the infrastructure gets built. GPUs don't generate revenue forever. People do.

What If Distribution Is The Real Moat

Look at Microsoft. Nobody opens ChatGPT because they need to finish a quarterly report. They open Word. Copilot simply appears inside a habit that already existed. The distribution was already won years ago.

Look at Meta. People don't wake up wanting an AI assistant. They wake up checking WhatsApp, scrolling Instagram, replying on Messenger. AI doesn't have to convince billions of people to change their behaviour. It only has to quietly improve something they're already doing.

That's an entirely different customer acquisition strategy. Actually, it isn't customer acquisition at all.

The Most Important Difference Might Be This

Infrastructure gets sold. Distribution gets monetized, over and over again.

A GPU is purchased once. A server gets installed once. A data centre eventually reaches capacity, and the next wave of growth usually requires building another one, which means another huge capital bill.

Distribution doesn't really work that way. Every Office subscription renewal, every AI-generated recommendation, every improved advertising impression, every AI-assisted search, every inference request, they're all monetised inside products people were already using yesterday. No new customer, no new marketing campaign, no new hardware purchase. Just better economics on an audience that already exists. That's a very different compounding engine.

So, Why Aren't These Companies Trading Like It

This is where things become interesting. Microsoft and Meta don't trade at the kind of premium many investors might expect from companies sitting at the centre of AI distribution.

There are perfectly reasonable explanations. Execution risk, massive capex, questions around Copilot adoption, concerns over monetisation timelines. Those concerns are real.

But it's also possible the market is simply moving in sequence. First it priced the infrastructure. Eventually it may decide to price the distribution layer. Markets rarely price every stage of a technology cycle at exactly the same time.

That Doesn't Mean The Thesis Is Risk-Free

None of this is guaranteed. Copilot still needs broader adoption. Meta still has to justify enormous AI investment. Infrastructure demand may remain stronger for longer than many expect.

And perhaps most importantly, if frontier models stop improving meaningfully, distribution won't matter nearly as much. Without compelling AI, even the best distribution network has less to distribute. That's an important counterargument.

The Next Question For Investors

For the last two years, the market has mostly asked who builds AI. That was probably the right question. The next one might be different: who actually owns the customer once AI becomes invisible.

History has often shown that building the technology and owning the distribution are two completely different businesses. And sometimes the second one turns out to be the better business.

Pulse24 Perspective

The AI story may not end with the companies building the biggest models. It may eventually be defined by the companies that make AI feel so natural that users forget they're using it at all. That's the transition we'll be watching closely.

How we read the data

Curious how we get from raw data to a take like this? Our Trader's Toolkit walks through the tools we lean on.

Explore the Toolkit